The S&P500 is arguably the most watched and talked about index in the world. In addition to being an index, it also a very liquid and tradeable security in the case of both the Exchange Traded Fund $SPY, Futures contract $ES_F and extremely liquid options contracts across strikes and expirations. For us who look at the entire world and all asset classes, not just stocks, the S&P500 is simply one index, in just one country, in just one asset class on earth. There are a lot more countries, a lot more asset classes (outside of stocks) and a lot more out there that is actually trending. The S&P500 is and has been in a sideways trend all year. Let’s break it down.

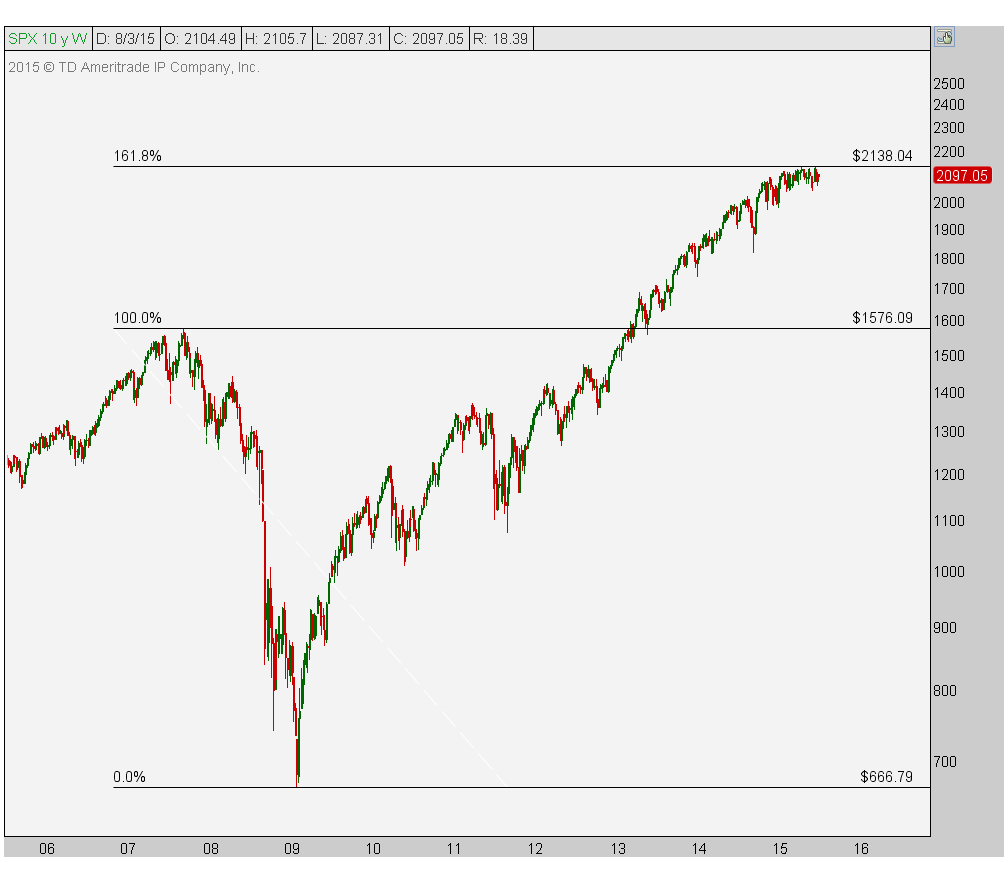

First of all, we need to get some perspective in terms of where we are bigger picture. We always like to start with a bird’s-eye view and then work our way down. Here is a weekly chart of the S&P500 going back 10 years. The market literally stopped going up as soon as it reached our 161.8% Fibonacci extension target from the 2007-2009 decline. This is an important level that the market is clearly acknowledging. You cannot argue that, so we won’t:

Now that we have some perspective, the S&P500 is in a tremendous bull market that is now about six and a half years old. Bigger picture, in order for me to be convinced that putting new money to work makes any sense at all up here, we want to clear this important extension target and the market needs to prove that it can hold above it. In the meantime, our stay away approach is still best.

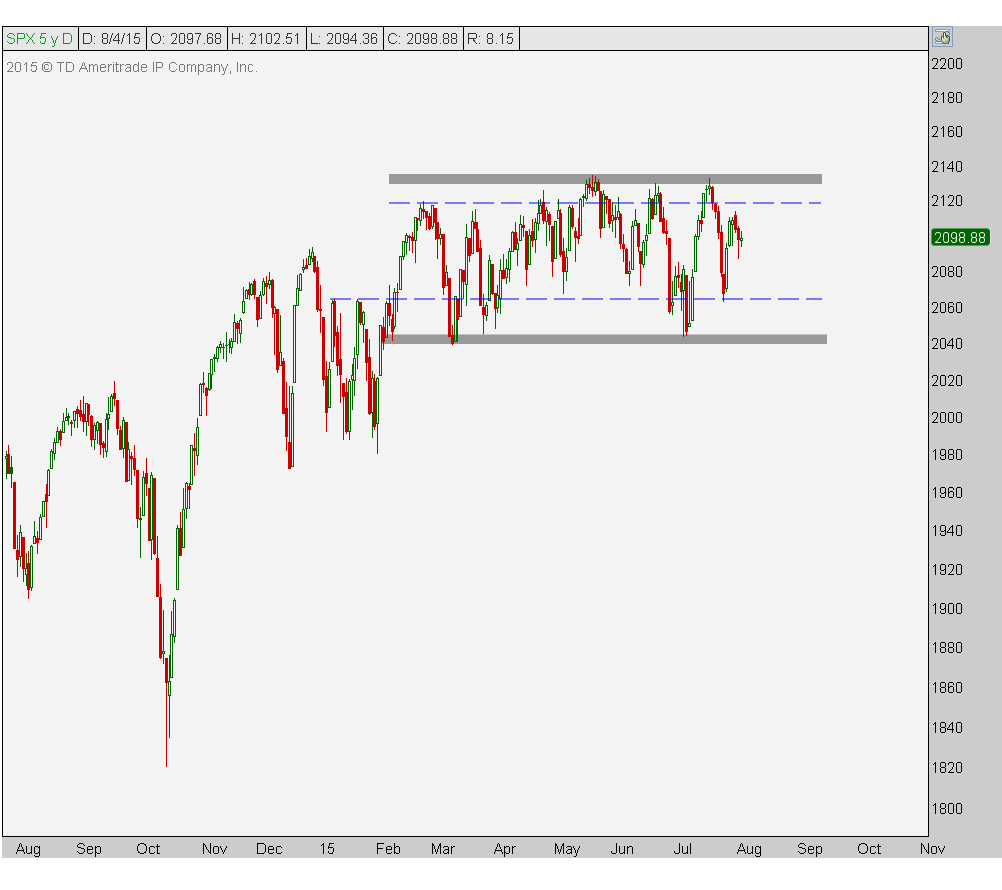

Shorter-term, however, there are some interesting developments that we have seen throughout the year that I think are worth mentioning. The first thing that stands out is the lack of trend in 2015. We are within a very well-defined sideways range that has screamed to stay away, particularly within the context of the weekly timeframe already achieving its upside objective:

From an absolute perspective, we are looking at about 100 point range, but I also included two horizontal support and resistance levels that have proven to be important as well along the way. These levels represent more of a tighter 50-60 point range. This is not an exact science and more of an art, so I don’t think there is a right or wrong answer here. But it cannot be argued that there is any kind of trend here over the short-term other than sideways.

The internals of the market, however, have shown deterioration throughout the sideways range that cannot be seen simply in a price chart. While the media obsesses over a 200 day moving average, we prefer to look within the index to see what is actually going on, rather than focusing on an invisible line. For the record, we do use a 200 period moving average to assist in trend recognition. When a security is trading above its 200 day moving average, for example, it is most likely not in a downtrend. Here is a chart of S&P500 stocks above their 200 day moving averages. Notice how as time has gone on, fewer and fewer stocks are in “uptrends”:

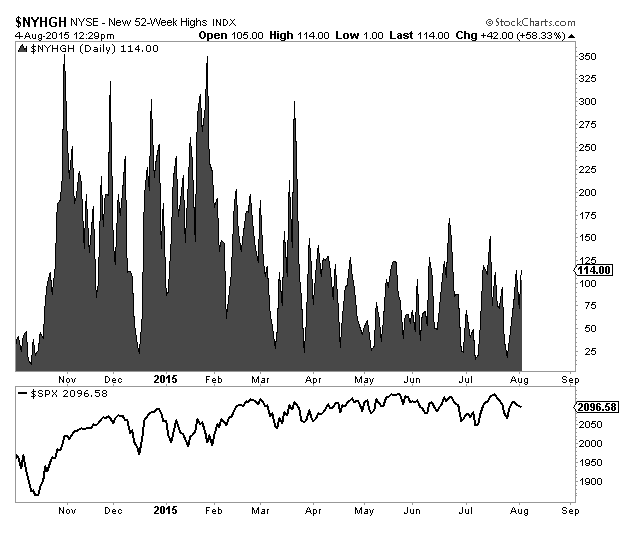

Currently just over half the S&P500 stocks are in uptrends, which is coming off its lowest levels since last Fall. Another way to judge the market’s breadth is to calculate the amount of stocks that are hitting new 52-week highs simultaneously with the index itself. Throughout the summer, the S&P500 has bumped up against all-time highs several times. Meanwhile, there are fewer and fewer stocks hitting new highs. Remember, although this index represents the market, it is a market of stocks. Collectively the amount of NYSE stocks hitting new highs is not telling us the same thing that the overall market has been signaling:

We can see that throughout this sideways consolidation, fewer and fewer names are hitting new highs as the S&P500 has hovered near all-time highs all year.

So what’s the conclusion? I can make an argument that this sideways correction is much healthier that if the market corrected through price. Markets can correct in one of two ways: through price or through time. Component-wise, half of the S&P500 stocks have already corrected by 10% from their respective peaks. We have seen sector rotation throughout this entire consolidation. As money has come out of Energy and Materials, for example, we have seen money flow into Healthcare and Consumer names, both Discretionary and Staples. I can’t take this as a bad thing.

How do we execute going forward? I still think this overhead supply is too much to ignore until the market proves it can be break through it. Regardless of the Fibonacci extension target being hit, regardless of the breadth of the market deteriorating, we are still within a sideways range, period. Price is the only thing that pays, so that’s always indicator #1. Until this resolves to the upside I would continue to stay away. A smart trader once told me, “If you trade the averages, you get average returns”. I have to agree with that, but even more so when the market lacks a trend direction.

The answer? It’s not a sexy one, but it’s what I think: I would focus on individual names and sectors, and other asset classes and countries other than U.S. stocks until a resolution out of this consolidation has been confirmed. These are the cards we’ve been dealt. We can’t trade the market we want, we have to trade the market we have.

No comments:

Post a Comment