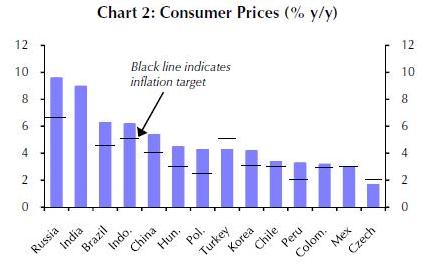

Capital Economics argues that while inflation is above official target levels in 11 of the 14 largest EMs (see chart) and will edge higher in coming months it should peak in the fourth quarter.

An official report from Brazil on Monday adds weight to the argument, with the central bank saying that economists are reducing their forecasts for inflation to 6.33 per cent for CY 2011, down from 6.37 per cent last week. It was the first reduction in nine weeks.

Global commodity price increases are still working their way along the economic chain pushing up inflation. But the cycle should soon be complete. Capital Economic says:

Even if global commodity prices now simply stabilise at their current high levels, food and energy inflation should still start to fall by around Q4 of this year. But if last week’s drop in oil prices proves to be the start of a series of falls in global commodity prices, as we think likely, food and energy inflation could drop sharply next year.

Either way, the key point is that the unwinding of the commodity price shock, coupled with a more general slowdown in the global economy, should lead to a fall in headline inflation in most emerging markets next year.

Capital Economics – not known for being bullish – admits there are domestic inflationary pressures in some countries, including Indonesia, India, Turkey and Brazil. But China is less vulnerable. And overall the scene is set for an eventual recovery in investor sentiment towards EMs.

The upshot is that the inflation fears that have spooked financial markets in emerging economies over the past week or so are ultimately likely to prove short-lived.For HSBC Asset Management this is is too optimistic. In a report published last week, entitled “Who let the tigers out?”, Philip Poole, global strategy head, quotes approvingly from Wen Jiabao, the Chinese prime minister. “Inflation is like a tiger: once set free it is very difficult to get back into its cages,” said Wen in March – and Poole seems to agree.

Other headwinds remain – most notably fears for the global recovery. But with growth in the developed world likely to remain sluggish, the hunt for higher returns should eventually pave the way for a renewed influx of capital to emerging markets and thus further gains for EM equities and bonds.

First, he says, the upswing in commodities is “more trend than cycle” driven by EM demand for energy, materials and food. Next, the second-round effects of inflation – in which domestic companies and workers participate by pushing up prices and wages – are serious. Shortages in capacity and skills mean EMs are far more prone to such pressures than DMs. He argues:

This creates the risk that in emerging economies inflation shocks turn into self-perpetuating inflation processes as expectations adjust higher and become embedded.Finally, EM central banks’ ability to control inflation through interest rate increases is damaged by the US Federal Reserve sticking to very loose monetary policies. So instead of raising rates, central banks are turning to controls on banks, but it is unclear whether this will work. The longer central banks put off interest rate increases “the bigger the risk they slip behind the curve in combating inflation.”

For Capital Economics, the implications for investors are straightforward – buy EM stocks and bonds, taking advantage of market dips. For HSBC AM, with its longer-term concerns about inflation, there are no simple answers. Poole suggests buying asset-intensive sectors including banks and minerals groups. He backs Russia (energy-rich, prospects for rouble appreciation) and Latin America (agricultural commodities). In Asia, he likes asset-intensive companies in South Korea, Taiwan and Hong Kong. Meanwhile, bond investors can look at EM index-linked offerings.

No comments:

Post a Comment